Have you ever heard of the insurance terms vertical exhaustion and horizontal exhaustion? If not, you’re not alone. That being said, they are once again a hot topic of conversation, so I think it’s important to take a look at them and how they may impact your business.

But first, I’d like to note there’s a lot of legalese involved, so it can get a bit complicated. If at any point you have a question on any of this, please don’t hesitate to reach out to us!

OK…now, on to the explanation!

What Is the Difference between Vertical and Horizontal Exhaustion?

In text form, here are the definitions:

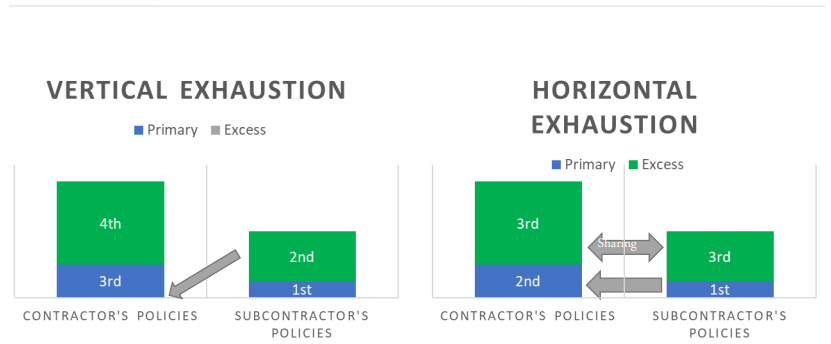

Vertical exhaustion allows an insured with multiple primary and excess policies covering a common risk to seek coverage from an excess insurer as long as the insurance policies immediately beneath that policy (as identified in the excess policy’s declaration page) have been exhausted, regardless of whether other primary insurance may apply.

Horizontal exhaustion is when all primary commercial general liability policies available to an insured must be exhausted before any excess or umbrella liability will contribute.

If you’re a visual learner, the following graph from Strafford helps explain the differences:

(click graph to enlarge)

States Have Differing Views of Vertical and Horizontal Exhaustion

States are split on the application of the different legal theories for assigning priority of insurance coverage. Virginia, Texas, Arkansas, Kentucky, and Missouri favor vertical exhaustion while Illinois, New Jersey, New York, and historically California have favored horizontal exhaustion.

Montrose Decision 1995 and 2020

The topic of vertical and horizontal exhaustion has a lot of history in our court system, particularly as it pertains to construction.

Commercial general liability (CGL) and excess/umbrella liability insurance are usually triggered when an injury or property damage takes place by an accident or occurrence. When the injury or damage takes place over an extended period of time, determining the trigger can be difficult.

In 1995, after reviewing a lower court decision of Montrose Chemical Corp. of California V Admiral Ins. Co., the California Supreme court adopted the “continuous trigger” theory deciding that “bodily injury or property damage that is continuous or progressively deteriorating throughout successive policy periods is potentially covered by all policies in effect during the periods of injury or damage continued to occur.” This presents potential tail exposure for continuing loss.

As a result of this decision, the CGL policy restricts coverage for damage that occurs over multiple policy periods to those policies where the insured wasn’t aware of the occurrence at the inception of the policy period.

Initially, in 1998, this was accomplished by ISO offering an endorsement to be attached to the form restricting coverage and then accomplished by the ISO CG 00 01 form being amended to include the verbiage in 2001. Not all endorsements or forms are the same, and some insurers will exclude any progressive or continuing bodily injury or property damage that starts before the CGL policy inception, whether any insured knew of the prior bodily injury or property damage.

In April 2020, the California Supreme Court, in the case of Montrose Chemical Corp. v. Superior Court of Los Angeles County, adopted a rule of vertical exhaustion applying that the policyholder only needs to exhaust the direct underlying excess policy before accessing the next layer of excess coverage thereby rejecting “insurers’ long-argued efforts to require policyholders with continuous injury claims to exhaust each layer of coverage for all years before accessing the next layer of excess coverage.”

This 2020 case is limited to excess policies covering continuous and progressive loss and declined to address “when or whether an insured may access excess policies before all primary insurance covering all relevant policy periods has been exhausted.” Additionally, it didn’t address horizontal versus vertical exhaustion in the additional insured context.

Horizontal and Vertical Exhaustion in the Additional Insured Context

Anyone who reads/reviews insurance requirements regularly in construction contracts knows that most upstream parties (owners and general contractors) dictate a specific amount of insurance be available to them from lower-tier subcontractors on their project. They also require this insurance to be primary and non-contributing through all their layers. This is great in theory, but when these two legal theories come into conflict, it can be a difficult process in a claim situation.

Horizonal exhaustion may leave a downstream party exposed to a breach of contract claim by an upstream party. It’s based on strict interpretation of the law, so amending policies to reflect party intent could be of great benefit to the downstream party.

Vertical exhaustion considers indemnity and insurance risk transfer as a whole. There is greater emphasis on intent, but each state and each situation must be looked at independently to ensure you are achieving adequate protection.

So, What’s the Solution?

Here are a few items your organization may want to look at now.

Contract Language

Ensure subcontract agreements require the owner, general contractor, and/or construction manager to be named as additional insureds, including completed operations, on a primary and non-contributing basis on the CGL and excess liability policies. This may require some customization of coverage to an insured’s policy(-ies).

Policy Language

Review all form and endorsement language (i.e. additional insured) to ensure privity of coverage is granted for upstream parties and have an awareness for any endorsements that don’t grant privity of coverage (for example: any endorsement that uses language such as “when you and such person,” or “for whom you are performing work for”).

Project Insurance

Project insurance should be considered to ensure adequate limits, coverage and terms and conditions for all parties.

Education Is Key!

Indemnification laws, state laws, and court rulings all have the potential to impact contract and insurance contract application. Educating yourself and having an understanding how to protect your organization from gaps in coverage and contract language can affect how choices are made to transfer risk.

Like I said, I realize this is an incredibly complicated topic. So, if at any point you have questions or need help, please don’t hesitate to reach out to us!