The 2017 string of natural disasters will go down as one of the most expensive in U.S. history with insured losses estimated to reach between $70-100 billion after storms and wildfires hit Texas, Florida, Puerto Rico, and California, respectively. How might this relate to stop loss insurance for healthcare? Well, employers buy protection for large health claims above a certain pooling or stop loss level to smooth out unforeseen losses in their health plan. A portion of those large catastrophic claims then get ceded to many of the same reinsurance markets that could face ratings downgrades, capacity, or balance sheet issues associated with the losses from 2017. When stop loss carriers cede their largest losses to reinsurers…we call these the “big cats”!

Roughly about 5 percent of the plan participants will generate 50 percent of the claims in a health plan. For an employer that is self-funded, most employees are unaware their employer buys stop loss insurance to cover large claims. This year, our Benefits Consulting Group and our Innovative Captive Strategies team were approached by a group of large national employers to explore forming a captive for the purposes of insuring stop loss insurance. Some of them had experienced a claimant or two that exceeded $1MM. An employer has a 6 percent probability of seeing one each year. The interest in our captive was to create a more efficient stop loss market and smooth out fluctuations from year to year. This was a welcome alternative from the double-digit premium increases and knee-jerk reactions they were experiencing in the retail marketplace.

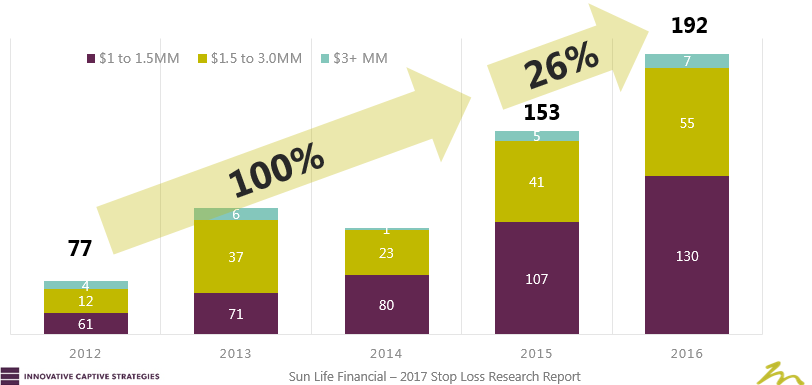

During this project, we illustrated what has transpired in the big cat marketplace since the “Affordable” Care Act (“ACA”) was implemented. As you will recall, the law restricted the use of lifetime maximums in health plans. The following chart illustrates the number of stop loss claimants from 2012 through 2016 that had paid health claims of $1MM or more. Our firm studied a data set comprised of 4.6MM covered lives representing 6.1BB in health plan spend since 2012. Shockingly, the claimants doubled from 2012 through 2015 and then by another 26 percent in 2016. The full year 2017 report will be released in the Spring of 2018.

What types of claims become “big cats”? Consistently, malignant neoplasms (cancer) remains the most dominant disease, accounting for about 27 percent of all stop loss claims, with leukemia, lymphoma, and multiple myeloma (cancers) running second. Kidney disease and ESRD ranked third with premature babies and transplants rising to the number four and five positions, respectively, based on stop loss reimbursement payouts.

So, what can an employer do to tame these cats? You’ll have to tune in to another edition of ‘What Up Holmes’ to find out. Here’s the good news…Holmes Murphy can hear these cats purring before they roar and help you act before they pounce.